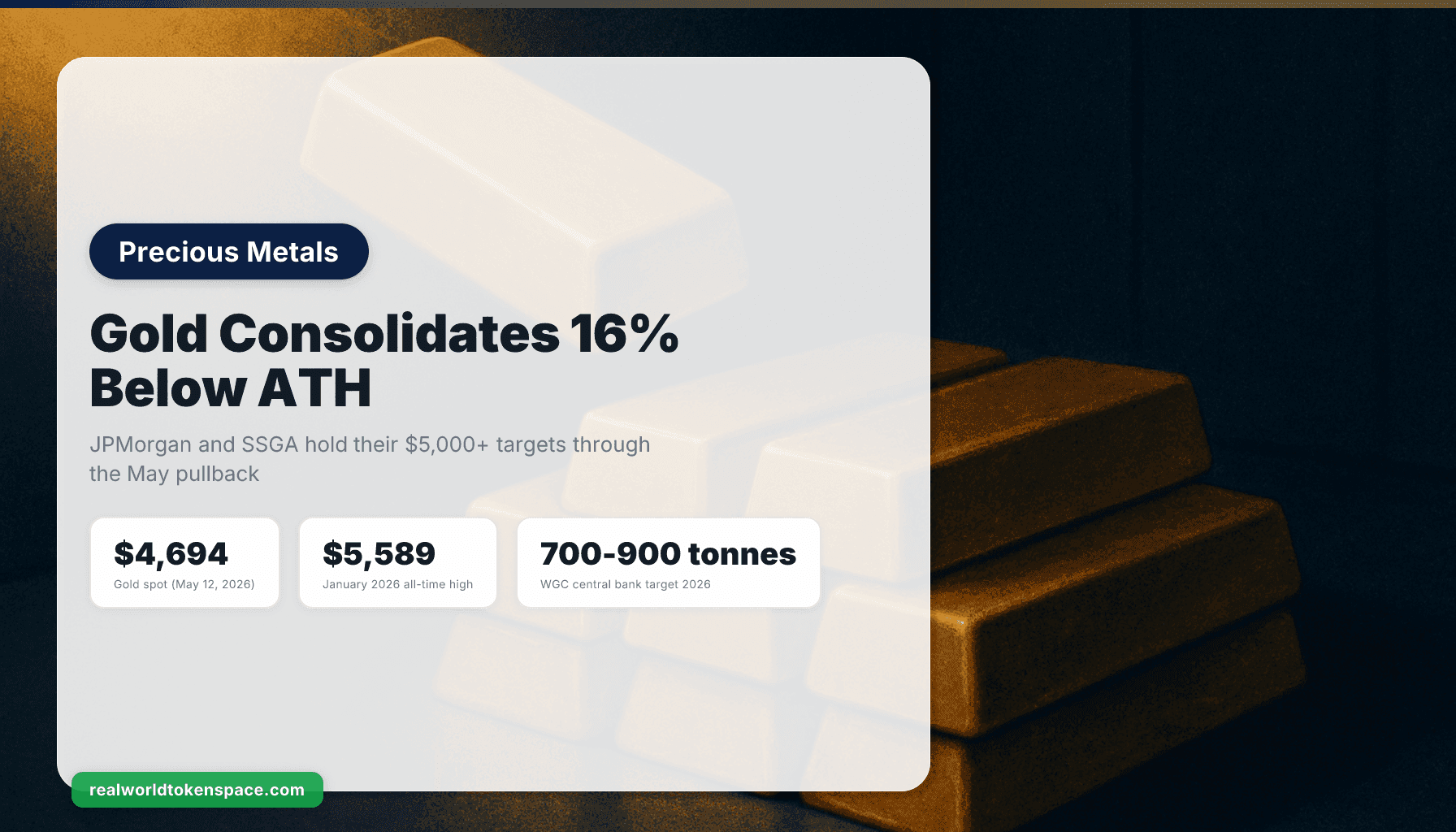

Gold closed at approximately $4,694 per ounce on May 12, 2026, roughly 16% below the January 2026 all-time high of $5,589. The pullback has been steady and uncrowded, a consolidation rather than a reversal, and the institutional desks that called the move higher in 2025 are not stepping away from the higher targets they published earlier this year. The World Gold Council reported 244 tonnes of net central bank buying in Q1 2026, a 3% year-over-year increase, and reaffirmed a full-year target range of 700 to 900 tonnes. JPMorgan Global Research and State Street Global Advisors, in their May 2026 outlooks, continue to position above $5,000 as the base-case path for the second half of the year. The physical bid did not leave. It paused.

The structural reads behind those calls have not changed. Central bank reserve allocation away from dollar instruments is the dominant macro story, and the WGC's full-year 2025 print of approximately 1,037 tonnes of net official buying was the largest annual total since 1967. JPMorgan's most recent commodities note frames the consolidation as a pause within a multi-year reallocation cycle, not as the end of it. SSGA's monthly gold monitor for May reads the price action as inventory rebalancing among Western tactical funds while Eastern central bank flows continue underneath. Neither desk is treating the $895 distance from the January peak as a signal that the thesis broke.

For stackers, the math at $4,694 is the math that always mattered. The ounce in the safe is the ounce in the safe. The dollar price of that ounce moves; the ounce does not. The 16% pullback from a record high is uncomfortable for anyone who bought the January candle, and entirely irrelevant to anyone who has been adding monthly. Physical first. The numbers we cover next are about tokenized allocated holdings that augment, never replace, the stack in the safe.

What the Mechanism Looks Like at $4,700

The lever connecting the consolidation to a resumption of the move is not paper speculation. It is the real-yield path. Gold trades inversely to real Treasury yields with a long lag, and the post-Fed-pause environment has compressed the real-yield ceiling while the term premium has reset modestly higher. Each piece moves the price calculus by a small amount. The WGC's Q1 demand trends note attributes the bid to two converging flows: official sector reallocation (the central bank story) and bar-and-coin demand from Asian retail (the household savings story). Both flows are price-insensitive within reasonable bands. They do not chase candles. They allocate.

The consolidation phase is what JPMorgan calls the digestion period. Tactical longs that crowded into the January breakout are being released, and the marginal seller is a Western fund desk rotating into equities, not the marginal buyer disappearing. SSGA's monthly monitor names the mechanism explicitly: when ETF flows go negative while official sector flows stay positive, the price compresses but the floor lifts underneath. The May print on GLD holdings will be the tell. If GLD continues to bleed while the WGC's monthly central bank data shows continued net additions, the consolidation is what it looks like. If both turn negative at once, the picture changes.

The Conditional Framing

If gold holds above $4,500, the WGC's 700 to 900 tonne 2026 thesis stays intact and the JPMorgan and SSGA $5,000+ targets remain the path of least resistance for the second half. The consolidation completes, ETF positioning resets, and the next leg is led by another central bank monthly print or a real-yield compression event.

Below $4,400, the dollar-strength bid takes over and the consolidation becomes a deeper correction. The 200-day moving average sits in that zone, and a break would force a re-rating among the tactical desks even if the physical bid remained intact. The WGC thesis would survive numerically (central banks would still be buying), but the price path would extend into the third quarter before any retest of the January high.

Between $4,500 and $4,700, the market is doing what it has done in every prior multi-year cycle: pausing while the physical layer absorbs the slack. Allocators rotated into gold through 2024 and 2025 are not panicking. The bid in Shanghai and Mumbai has not gone away. Traders focused on the COMEX tape see open interest still elevated and the December contract structured in modest contango, which is consistent with a pause rather than a breakdown.

The Tokenized Layer at This Price

For stackers who already hold physical and want a small allocated, audited, redeemable holding on Ethereum for fractional ownership, 24/7 liquidity, or programmatic settlement, three tokenized gold products clear the RWTS Trust Score threshold for Tier 1.

$KAU (Kinesis): Trust Score 92, Tier 1. 1 gram allocated, Brink's vaulted, monthly attestations, redeemable in physical at the Kinesis vault network. The Trust Score sits at the top of the gold token set because of the Brink's custodian relationship, the redemption mechanics, and the monthly third-party audit cadence.

$PAXG (Paxos Gold): Trust Score 89, Tier 1. 1 troy ounce allocated, LBMA Good Delivery bars vaulted in London, NYDFS-regulated issuer, redeemable in physical at the Paxos vault. The Trust Score reflects the regulatory wrapping, the LBMA-grade backing, and the longest operating track record of any tokenized gold product.

$XAUT (Tether Gold): Trust Score 86, Tier 1. 1 troy ounce allocated, Swiss vaulted, monthly attestations published by an independent auditor. The Trust Score is the lowest of the three Tier 1 options because of the issuer concentration and the more limited redemption network, but the LBMA Good Delivery backing and the public attestation cadence keep it in the top tier.

None of these is a recommendation to substitute tokenized holdings for physical. They are an augmentation layer for the portion of an allocation that benefits from being on-chain. A stacker who wants to maintain a 95% physical / 5% on-chain split for liquidity reasons gets a different answer than a fund treasury looking for a regulated tokenized holding that settles in seconds. Both are valid. The Trust Score is the input, not the decision.

Where We Sit

The consolidation at $4,694 is doing what consolidations do. Central bank buying remains the structural floor and the WGC's 700 to 900 tonne range is intact. JPMorgan and SSGA continue to hold $5,000+ as base cases. The marginal seller is a tactical Western fund, not the structural buyer. Imagine what happens if the May central bank print comes in above the trailing twelve-month average. Imagine what happens if it comes in below. Both are possible. The conditional structure tells you what to watch.

RWTS isn't bullish or bearish on gold. We're the credit-rating agency for tokenized real assets. We rate. You decide.

Not financial advice.