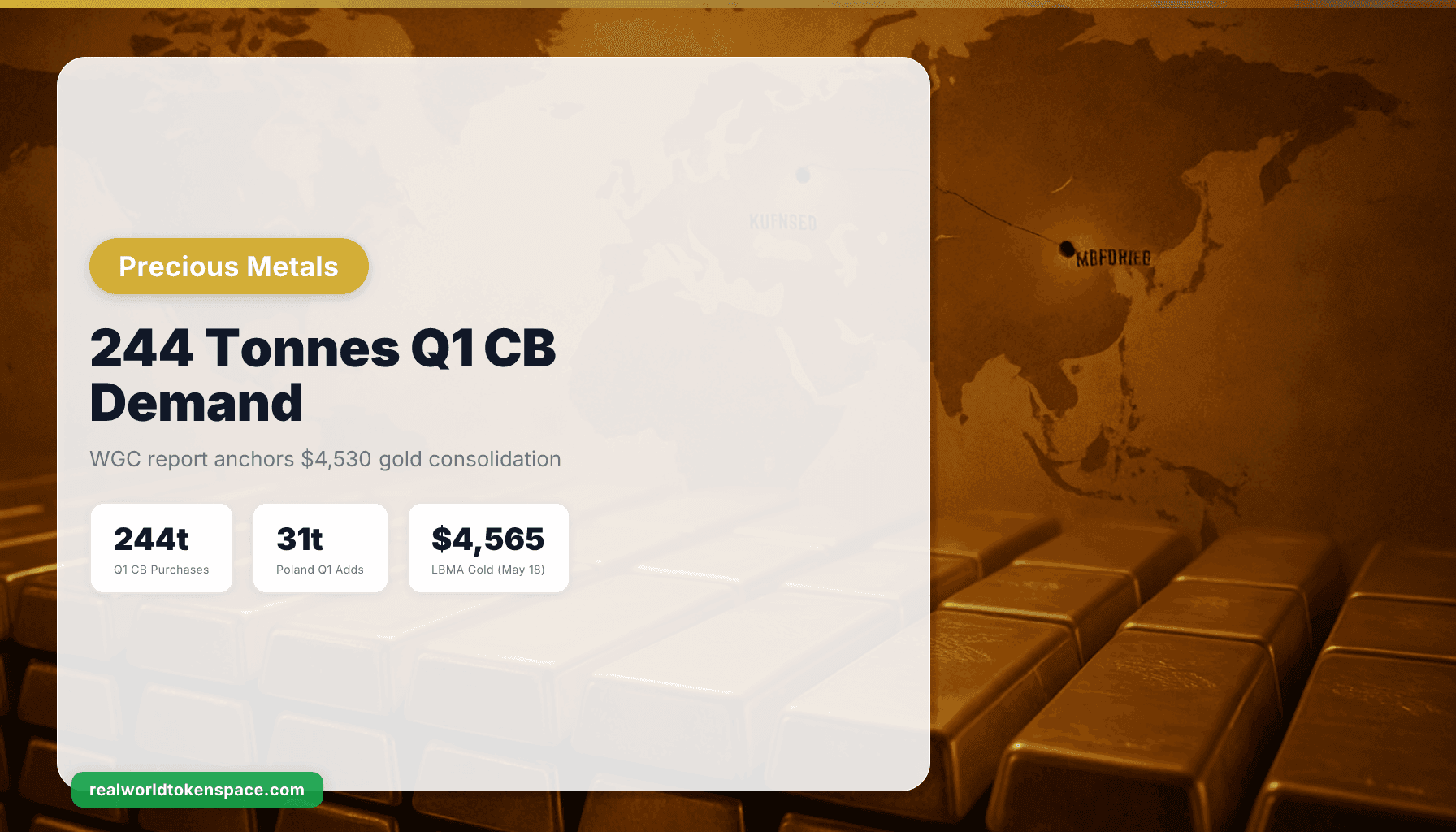

WGC Reports 244 Tonnes Q1 Central Bank Gold Demand as Spot Consolidates $4,530

Central bank gold demand began 2026 strongly, with estimated net purchases of 244t in Q1. Demand exceeded both the previous quarter and the five-year average, underscoring continued commitment to strengthening reserves with gold.

The current live gold spot price is $4537.56 per fine ounce. On May 18, 2026, LBMA Gold Price stood at $4,565.40. The metal is holding a $4,530–$4,565 range after retreating from April highs above $4,700, as the yield on US 10 Year Note Bond Yield eased to 4.63% on May 20, 2026 following weeks of pressure from the yield on the US 10-year Treasury note held its recent advance to around 4.67% on Wednesday, hovering at 16-month highs as growing concerns over an energy-driven inflation shock fueled expectations that the Federal Reserve could raise interest rates.

The Physical Reality: Warsaw, Beijing, and Vault Flows

The National Bank of Poland was once again the largest purchaser, increasing its gold reserves by 31t over the quarter to 582t. Despite recent statements from Governor Adam Glapiński about the possibility of selling some of its gold, the central bank appears to remain focused on reaching its 700t target.

The People's Bank of China increased its gold reserves by 7t in Q1, more than doubling its net purchase in the previous quarter (3t). This lifts the PBoC's total gold reserves to 2,313t (9% of total reserves).

Poland is leading global gold accumulation in 2026, adding over 20 tonnes, more than any other central bank so far this year. Poland is leading global gold accumulation in 2026, adding over 20 tonnes, more than any other central bank so far this year. This purchase is part of a broader multi-year plan to reach 700 tonnes, reflecting heightened security concerns on NATO's eastern flank.

The World Gold Council's institutional weight matters here because its Q1 data captures reported and estimated unreported official-sector activity. The quarterly figure reflects all available information and informed estimation of unreported activity, but the current environment of heightened geoeconomic uncertainty and more volatile gold prices may, therefore, increase the potential for future revisions. Based on the strong start to the year, we expect central banks to contribute meaningfully to global gold demand going forward, as geoeconomic uncertainty stays elevated and reserve-diversification incentives remain intact.

The RWTS Trust Score Angle: Tokenized Gold at Tier 1

For allocators evaluating tokenized gold, two Tier 1 tokens hold the highest RWTS Trust Scores among allocated products: Paxos Gold (PAXG, 8.4/10) and Kinesis Gold (KAU, 7.9/10).

PAXG represents allocated, London Good Delivery bars vaulted in Brink's facilities. Each token is redeemable for one fine troy ounce. Attestations are monthly via third-party auditors, and the issuer (Paxos) is regulated under New York State's trust charter. The 8.4 score reflects high reserve transparency, regulatory oversight, and established redemption mechanics. The slight deduction accounts for custodial concentration and the trust-based relationship between token holder and issuer.

KAU operates on a similar allocated model, with gold held in insured third-party vaults across multiple jurisdictions. The 7.9 score weights the distributed custody structure and redeemability mechanics, with minor deductions for lower liquidity depth compared to PAXG and slightly less frequent public attestation.

Both tokens augment physical gold ownership by enabling 24/7 tradability, fractional exposure, and integration into DeFi collateral and yield strategies. Neither replaces allocated bullion in a private vault, but both provide efficient on-chain exposure to physical gold price movements without futures roll costs or ETF management fees.

RWTS does not recommend either token. We score the reserve quality, auditability, and redemption infrastructure. The decision to allocate remains yours.

Mechanism: Why Central Banks Buy at $4,500+ When Target Returns Suggest Patience

While central bank demand remains high, the sharp price increase in gold simultaneously has a dampening effect. Higher prices make additional purchases more difficult and simultaneously change the weight of existing gold holdings within total reserves. This creates a tension for 2026 between structural buying interest and a price level that does not automatically facilitate new purchases.

The mechanism driving continued purchases despite elevated prices is reserve diversification away from dollar-denominated claims. China recorded the largest increase in gold reserves over the period, adding more than 350 tonnes. This move aligns with Beijing's long-running push to diversify reserves away from the U.S. dollar and reduce exposure to Western financial systems, reinforcing gold's role as a politically neutral anchor within global reserves.

When a central bank buys gold at $4,565 per ounce, it is not timing a trade. It is adding a non-sovereign, non-defaultable reserve asset into a portfolio otherwise composed of sovereign credit instruments (bonds) whose risk profile has been repriced upward by geopolitical fragmentation and sanctions use. Gold's opportunity cost falls when Treasury yields rise if those yields reflect inflation risk or credit risk rather than real return.

The World Gold Council forecasts central banks to purchase roughly 850 tonnes of gold in 2026 — almost the same as last year. At the same time, official-sector demand remains resilient in the first few months, according to the World Gold Council, which forecasts central banks to purchase roughly 850 tonnes of gold in 2026 — almost the same as last year.

If that thesis holds, Q1's 244 tonnes implies a run-rate modestly below target, but within forecast range given the lumpiness of reported flows.

We Rate. You Decide.

RWTS is not bullish or bearish on gold. We score tokenized products that reference physical ounces. PAXG and KAU both score Tier 1, with Trust Scores of 8.4 and 7.9 respectively, because they maintain allocated bullion in audited vaults with transparent redemption paths.

The World Gold Council's Q1 report confirms that central banks added 244 tonnes despite gold trading near $4,500–$4,600. Poland is accumulating toward a 700-tonne target. China continues slow, steady reserve expansion. The physical gold market remains anchored by official-sector demand, not speculative positioning.

Tokenization does not change the metal. It changes the settlement rail. The ounce in a Brink's vault backing a PAXG token is the same ounce a central bank would acquire through LBMA settlement. The difference is custody model, counterparty, and liquidity venue.

RWTS rates the tokenized structure. The allocation decision—physical, tokenized, or none—is yours.