DeFi Vault Yields Compress Below TradFi as Borrowing Demand Collapses

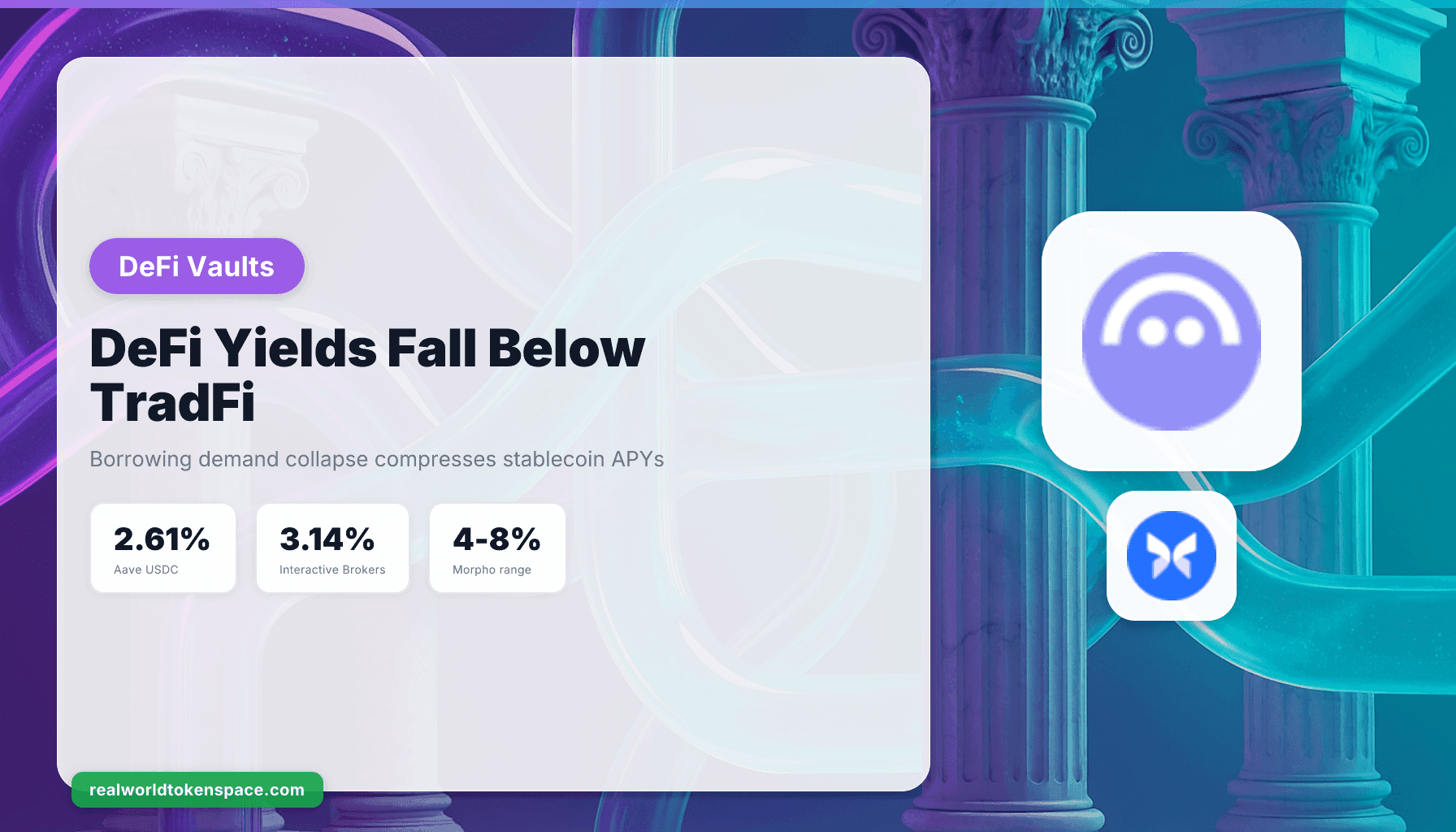

Flagship DeFi rates have fallen below traditional finance (TradFi), with Aave's 2.61% APY on USDC trailing the 3.14% offered by Interactive Brokers, as of April 2026. The crossover is a structural inflection point. For three years, DeFi lending offered a premium over risk-free rates, compensating depositors for smart-contract risk, custody complexity, and regulatory uncertainty. That premium has vanished as borrowing demand collapsed across the largest protocols.

Crypto investors who once turned to decentralized finance for easy passive income through juicy yields are running into a new reality: the numbers no longer add up, as DeFi's returns were more than promising in 2021-2022, reaching 20% on protocols like Aave, but money sitting in DeFi is now facing a higher risk for lower returns. The mechanism is straightforward. Lending protocols generate yield by matching depositors with borrowers. When borrowers disappear, yields compress to the marginal rate at which the remaining borrowers are willing to pay.

The Borrowing Demand Collapse

Aave frames the current weakness as cyclical rather than structural, pointing to unusually depressed crypto sentiment, with the Fear and Greed Index below its 2022 lows, as a key driver of reduced borrowing demand, which in turn weighs on deposit rates, with a spokesperson stating that stablecoin rates on Aave have largely tracked leverage demand. The explanation holds under scrutiny. Leverage demand drives borrowing. When traders exit positions, close loops, or move to the sidelines, the bid for stablecoin liquidity evaporates.

The alternative hypothesis is that DeFi never generated organic yield at scale. Instead, rates were subsidized by token incentives, recycled leverage, and speculative positioning that mistook beta for alpha. When those flows reversed, the sustainable rate revealed itself, and it converged toward the risk-free baseline rather than maintaining a persistent premium.

Paul Frambot, co-founder of Morpho, a lending infrastructure protocol, says this bleak outcome for yields was inevitable, stating that undifferentiated lending converges toward risk-free rates because when every depositor shares the same collateral, the same parameters, and the same outcome, there is limited room for specialization and returns compress. That framing shifts the conversation. If pooled models inevitably compress, then the product design itself constrains yield, and curated, isolated markets become the differentiation layer.

The Morpho Exception

Morpho, with over $10 billion in deposits, offers a different model, with its platform letting curators build lending vaults, essentially customized pools with their own risk parameters, collateral choices and yield strategies, managed by specialist teams rather than governed by a single set of rules, and bluechip stablecoin yields on Morpho are on average higher than in pooled models and backed by straightforward collateral like BTC and ETH. As of early 2026, Morpho Blue typically offers the highest supply rates for stablecoins (4-8% on USDC) because its peer-to-peer matching and modular vault architecture reduce the spread between supply and borrow rates, while Aave V3 generally offers 3-6% on USDC, and Compound III ranges from 3-5%.

The architecture matters. Morpho Blue is a permissionless base layer for creating isolated lending markets. MetaMorpho vaults sit on top, with curators allocating depositor capital across multiple Blue markets. Each market has one loan asset, one collateral asset, one oracle, one LTV, and one liquidation threshold. Risk is isolated. A problem in one market doesn't contaminate others.

Morpho is the biggest story in DeFi vaults right now, with the protocol's TVL above $9.5 billion through H2 2025 and sitting around $5.8 billion as of late February 2026 after broader market pullbacks, remaining the second-largest DeFi lending protocol behind Aave, and curators create a vault that deposits into multiple Morpho Blue markets, giving depositors diversified lending exposure while the curator manages which markets and how much goes to each. Curators include Gauntlet, Steakhouse Financial, RE7 Labs, and Block Analitica, each managing risk parameters and capital allocation strategies.

The Kraken DeFi Earn Case Study

Crypto exchange Kraken is rolling out a new DeFi Earn product in Canada, the European Economic Area, and most U.S. states, providing onchain earning opportunities, including APYs of up to 8%, with Kraken's DeFi Earn tapping vault infrastructure provider Veda to power the new product, with risk managers Chaos Labs and Sentora operating the first three USDC vaults, allocating funds to well-known onchain protocols like Aave, Morpho, Sky, and Tydro. Kraken's DeFi Earn product has passed 200 million dollars in deposits amid a rising demand for onchain yield that users can access from a regular exchange app, with the program running on three vaults provided by Veda, with more than 40,000 users now using these vaults through the Kraken app to earn yield on cash and stablecoins, with the product converting deposits into USDC and allocating them into onchain strategies.

The integration is a bridge. Kraken wraps DeFi vault infrastructure into a centralized exchange interface, abstracting wallet management, gas fees, and protocol selection. Users see a simple earn interface. Behind it, curators are routing capital to Morpho, Aave, and Sky based on real-time yield and risk parameters. The model scales DeFi access without requiring users to hold private keys or navigate smart contracts directly.

The "We Rate, You Decide" Anchor

RWTS isn't bullish or bearish on DeFi yields. We're the credit-rating agency for tokenized real assets. Aave's flagship USDC pool yields 2.61%. Interactive Brokers pays 3.14% on idle cash. Morpho curators deliver 4-8% through isolated markets with named collateral and transparent risk parameters. Kraken has onboarded 40,000 users to DeFi vaults by embedding Veda's infrastructure into its exchange app.

The mechanism is clear. Borrowing demand collapsed as leverage left the system. Pooled lending models compress toward risk-free rates when utilization drops. Curated vaults offer a structural alternative by separating the lending primitive from the risk management layer, allowing specialist teams to optimize for yield within defined risk boundaries.

The decision to rotate capital into DeFi, in what size, through which curator, and at what level of smart-contract exposure, is yours. We rate the products, publish the data, and flag the forks. You decide.