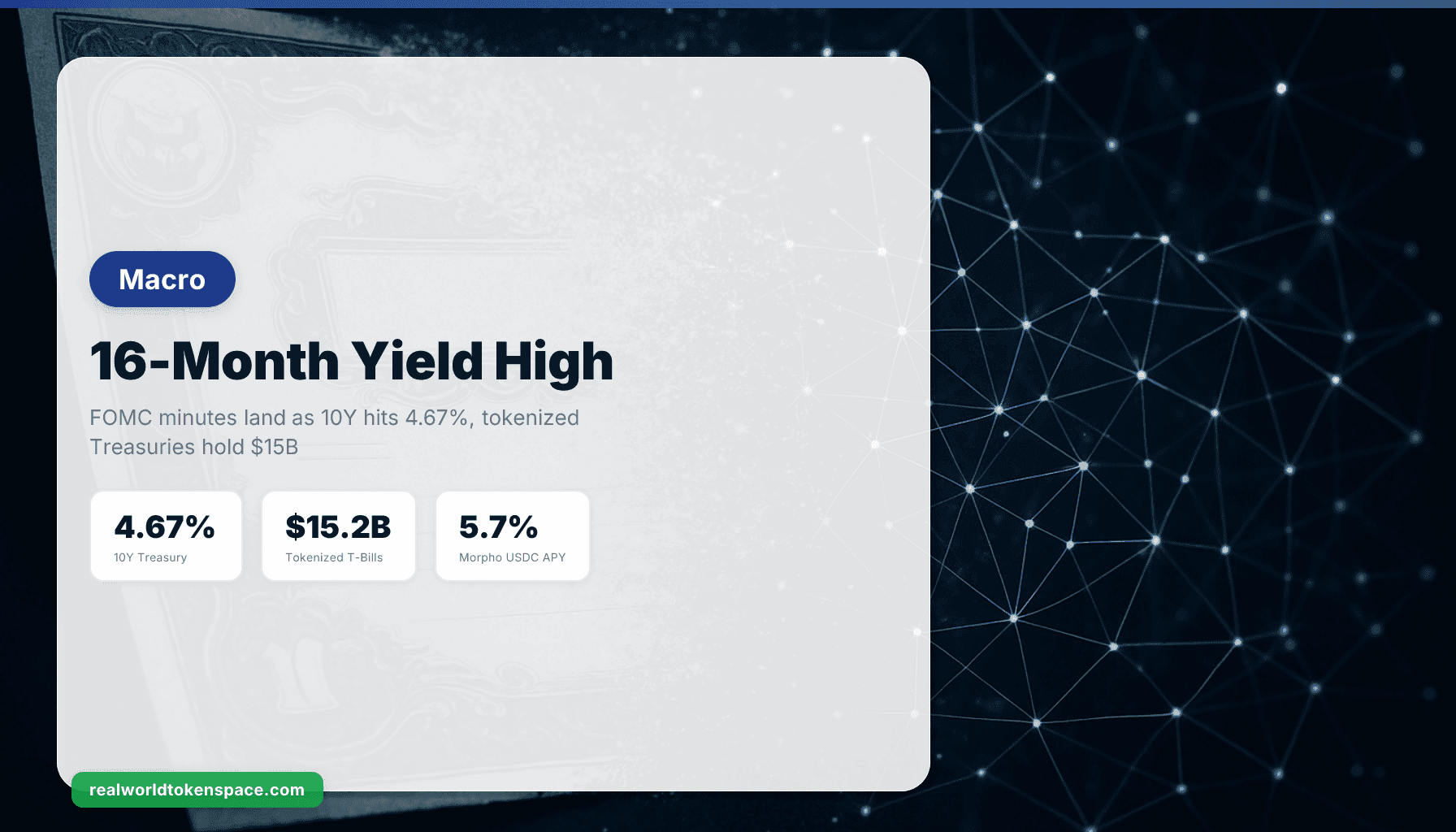

10-Year Treasury Hits 4.67% 16-Month High as FOMC Minutes Land: Impact on Tokenized Treasuries and DeFi Yields

The yield on US 10 Year Note Bond Yield eased to 4.63% on May 20, 2026, marking a 0.04 percentage points decrease from the previous session. But the intraday high story is more revealing: the yield on the US 10-year Treasury note held its recent advance to around 4.67% on Wednesday, hovering at 16-month highs as growing concerns over an energy-driven inflation shock fueled expectations that the Federal Reserve could raise interest rates.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 3‑1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

The Federal Reserve held rates at its April 29 meeting, and the minutes from that meeting were released today, May 20. Inflation is elevated, in part reflecting the recent increase in global energy prices. Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook. Inflation is elevated, in part reflecting the recent increase in global energy prices. Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook.

The mechanism driving the yield spike is clear: oil above $100/barrel from prolonged Strait of Hormuz closure is feeding through to consumer prices, and Long-term US Treasury yields surged, with that on the 10-year note rising to a 16-month high of 4.7% on Tuesday, and that on the 30-year bond reaching a 18-year high of 5.2%, amid an increasingly inflationary outlook.

Tokenized Treasuries: $15.2 Billion in Supply, Holding Steady Despite Yield Competition

The tokenized U.S. Treasuries sector has reached a historic milestone, surpassing $15.35 billion in total value locked (TVL) as of May 13, 2026. This new all-time high reflects surging institutional demand for on-chain, yield-bearing dollar assets amid persistent inflation concerns and macroeconomic uncertainty.

Tokenized U.S. Treasuries reached $15.20 billion at the start of May, led by Circle's USYC ($2.91B) and BlackRock's BUIDL ($2.58B), rwa.xyz shows. Circle's USYC is the largest product at $2.91 billion, followed by BlackRock's BUIDL at $2.58 billion.

As of mid-May 2026, USYC holds approximately $3.0 billion, BUIDL $2.6 billion. USYC$3.0B-0.34% BUIDL$2.6B+7.69% USDY$2.1B-0.19% iBENJI$1.5B+8.06% JTRSY$1.0B-8.87% WTGXX$950.6M-2.15% USTB$907.0M+2.21%

The RWTS Trust Score for USYC is 9.1/10 (Tier 1). It is issued by Circle (regulated, public reserve attestations), backed 1:1 by short-duration Treasuries and cash equivalents, with daily on-chain transparency. BUIDL scores 8.9/10 (Tier 1), issued via Securitize with BlackRock as the underlying fund manager, backed by Treasuries and reverse repo, with institutional-grade custody and regular attestation.

Both products offer 3-4% APY currently, derived from the short-end Treasury curve. That yield is now competitive with—or slightly above—many base-layer DeFi stablecoin lending rates, which have compressed as borrowing demand cooled.

DeFi Stablecoin Yields Compress as Marginal Borrower Recedes

Morpho USD Lending vaults currently offer 4-6% APY on USDC. The Gauntlet Core vault shows around 5.7% APY. Stablecoin supply yields currently range from 3-8% APY depending on protocol and market conditions, consistently outperforming traditional savings while carrying smart contract and market risk.

Aave, the largest decentralized money market, Aave is the largest decentralized lending protocol, holding over $27.8 billion in deposits as of February 2026. Its USDC supply APY sits in the 4–6% range depending on utilization. When the on-chain risk-free rate (tokenized T-bills at 3.5%) rises to within 50-100 basis points of the DeFi lending rate, the relative attractiveness of taking smart-contract risk for incremental yield diminishes.

Risk managers Chaos Labs and Sentora will also operate the first three USDC vaults, allocating funds to "well-known onchain protocols" like Aave, Morpho, Sky, and Tydro, which will provide variable returns "derived from genuine market demand paid by borrowers."

The causal chain is: higher Treasury yields → lower relative DeFi spread → reduced capital inflows to lending protocols → compressed utilization → lower APYs. When 10-year Treasuries yield 4.67% and 3-month bills yield ~3.8%, a 5.7% Morpho vault with smart-contract and platform risk offers roughly 190 basis points of spread. That is narrower than the 300–500 bp spreads seen when Treasuries were yielding 2–3% in prior years.

Exchange Yield Products: Kraken and Coinbase Adjust

If you hold USDC on Kraken, it earns automatically. By default, users earn 1.75% APR. For customers with Kraken+, rewards increase to up to 3.75% APR, without changing how your USDC works or where it lives.

Kraken launched automatic USDC rewards in early May 2026, offering 1.75% base and up to 3.75% for Kraken+ subscribers. That yield is sourced from Circle's partnership arrangements and platform lending activity. It sits below the Treasury curve at the short end but provides instant liquidity, which tokenized T-bill products (with T+0 to T+1 redemption windows) do not always match.

Coinbase's staking program supports Ethereum (ETH) at an estimated 2.31% annual percentage yield (APY) net of fees. Coinbase staking APYs include Solana (SOL) at 5.85% APY, Cardano (ADA) at 2.45% APY, Polkadot (DOT) at 9.31% APY, Tezos (XTZ) at 3.36% APY, and Cosmos (ATOM) at 11.38% APY.

Coinbase does not offer a native USDC yield product at the retail level (outside of institutional USDC lending on Base via Morpho integration), but it is positioning Base-native DeFi access as the yield rail for stablecoin holders who want on-chain returns.

Mechanism: Why Rising Treasury Yields Compress DeFi But Support Tokenized T-Bill Demand

When the 10-year yield rises from 3.5% to 4.67%, two forces act on on-chain yield products:

-

Demand for tokenized Treasuries increases because institutional allocators and DAO treasuries can now earn 3.5–4.0% APY in a fully reserved, regulatory-compliant instrument. USYC, BUIDL, BENJI, and USTB all benefit from higher short-end rates feeding through to their NAV yields.

-

Demand for DeFi lending decreases (or grows more slowly) because the incremental spread for taking smart-contract risk narrows. A Morpho vault at 5.7% offers 170 bps over USYC at 4.0%. When USYC was yielding 2.5%, that same vault at 6.0% offered 350 bps spread. The risk-adjusted return calculus shifts.

The April FOMC minutes reinforce this: Participants generally observed that overall inflation remained above the Committee's 2 percent longer-run goal. Some participants remarked that further progress in reducing inflation had been absent in recent months.

If inflation remains sticky and the Fed holds rates at 3.5–3.75% through year-end (as The Fed is still expected to keep the federal funds rate unchanged for the remainder of the year, although market-implied odds of a rate hike in December currently stand at around 50%.), then Treasury yields will likely remain elevated, and the on-chain yield landscape will stay bifurcated: high-quality tokenized Treasuries anchoring the floor, DeFi lending offering 150–250 bps premiums for protocol risk, and higher-risk strategies (Ethena, Pendle PT) offering structural yield for those willing to take duration, funding-rate, or liquidation risk.

RWTS View: The Yield Curve Now Runs Through Ethereum

Tokenized Treasuries crossed $15 billion because institutional allocators need dollar-denominated yield that settles on-chain, integrates with DeFi collateral, and clears 24/7. When the Federal Reserve holds rates at 3.5% and 10-year Treasuries yield 4.67%, that on-chain T-bill at 3.8% APY is no longer a novelty. It is a competitive cash-management instrument.

RWTS scores USYC 9.1/10, BUIDL 8.9/10, and USDC 9.4/10 (for reserve quality, regulatory standing, and liquidity). The scores reflect structure, not price prediction. The decision to rotate from DeFi lending into tokenized Treasuries—or vice versa—depends on your time horizon, liquidity needs, and risk tolerance.

We rate the products. You decide the allocation.