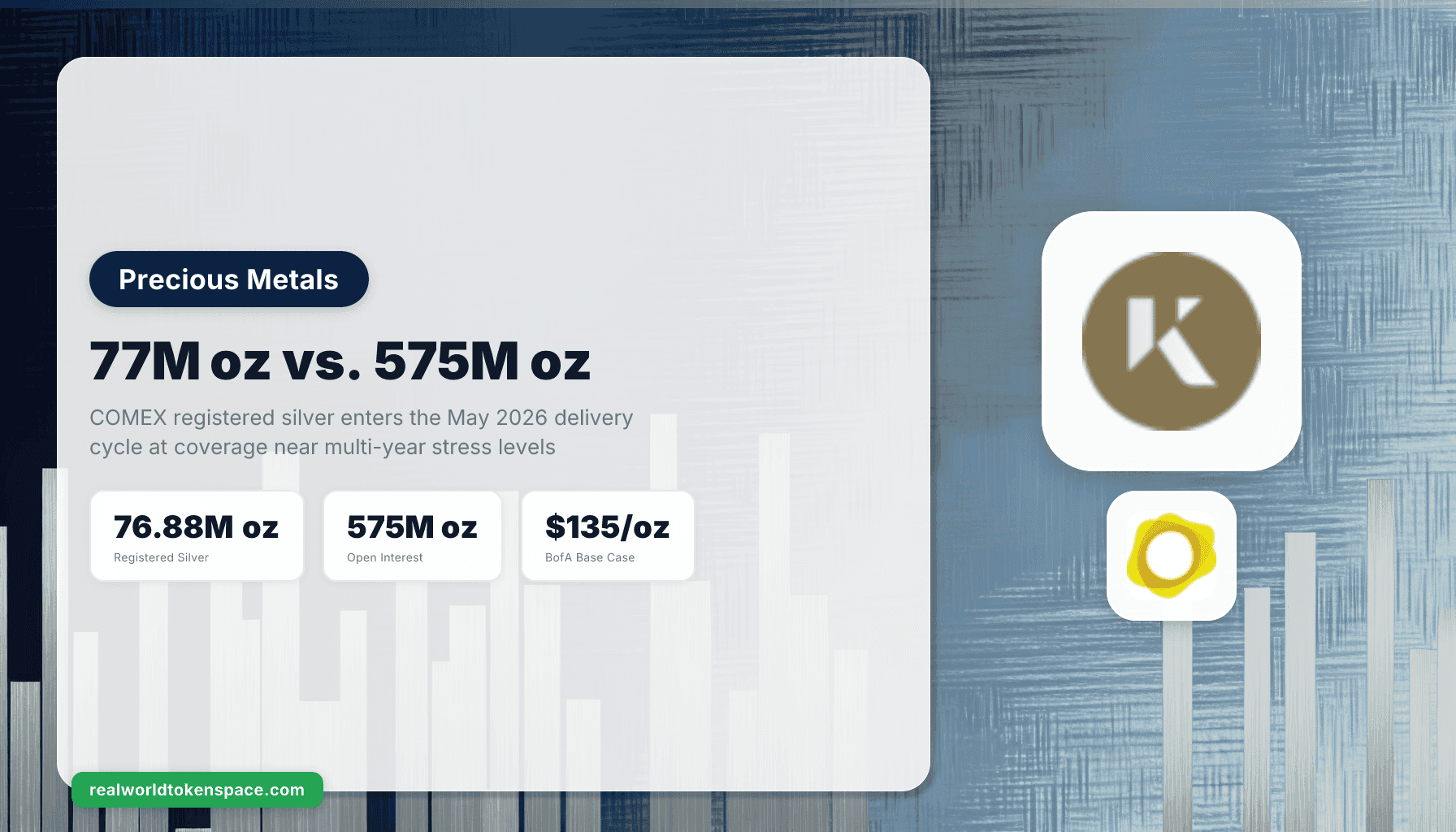

The May 2026 delivery cycle on COMEX silver is opening with a coverage ratio that has not looked this thin in modern memory. Per Sora Futures' April inventory note, registered silver inventory now sits at roughly 76.88 million ounces. Open interest on the silver futures complex sits above 575 million ounces. That is approximately 7.5 ounces of paper claim against every registered ounce in the vault, going into the contract month that historically delivers the most metal of the year.

The institutional citation that anchors this story is not RWTS analysis. It is the Silver Institute's World Silver Survey 2026, which projects a sixth consecutive annual deficit at 67 million ounces in 2026 against a 2025 actual deficit of 40.3 million ounces. Approximately 762 million ounces have already been drawn from above-ground stocks since 2021, per SchiffGold's exploring-finance Comex report. The metal is doing what stackers said it would do. The vault is doing what physics requires when the deficit runs long enough.

Bank of America commodities strategist Michael Widmer set a 2026 silver target range of $135 to $309 per ounce in his February outlook, with the base case anchored to gold-silver ratio compression toward 32:1 (the 2011 low). Spot silver hit an all-time high of $121.64 on January 29, 2026, then consolidated to $77 in mid-April. The delivery-cycle stress arrives into a market where the institutional price targets are no longer fringe.

The Physical Reality, Quantified

For 15 consecutive months through early 2026, physical silver left COMEX warehouses at a rate the exchange had not previously processed. December 2025 produced 65 million ounces of deliveries in a single month, a record. April delivery was lighter on the registered-eligible flow side, but the trend of metal leaving the warehouse system entirely has continued into Q2.

The math on May is what stackers and the futures desks are watching. Per Investing.com's coverage of the coverage ratio, each 1% increase in May delivery volume above historical norms requires an additional 5 to 6 million ounces of registered metal. At 76.88 million ounces of registered silver, a January-style delivery month at half the magnitude would draw down roughly 21% of registered inventory in a single week.

Registered silver has dropped over 70% from its 2021 peak. The inventory that remains is not idle. It is the physical anchor for a paper book carrying 7.5x leverage, in a market that has run a structural deficit for five years and is projected to run a sixth.

The Stacker Frame and the RWTS Position

The "if you don't hold it, you don't own it" axiom is the right starting point. A bar in the safe is the only silver position that has zero counterparty risk, zero rehypothecation risk, and zero settlement-failure risk. Physical first. That order does not change.

What does change is the question of what to do with the portion of an allocation that needs to settle, move, or earn alongside the bar. RWTS does not take a view on whether silver goes to $135 or $309 or back to $50. We do not take a view on whether the May delivery cycle breaks or absorbs. We rate the tokenized products that exist for the slice of capital that wants allocated, audited, redeemable silver in a form that can move on Ethereum or settle a card payment. You decide whether and how much of that slice fits your stack.

What RWTS Trust-Scores in Tokenized Silver Right Now

The two tokens that meet the RWTS bar for institutional review on the silver side are KAG (Kinesis) and the small set of allocated silver products that publish monthly attestation reports.

KAG represents 10 grams of allocated silver per token, vaulted with Brink's and audited monthly. It pays a yield denominated in additional metal, sourced from 15% of Kinesis platform transaction fees rather than from rehypothecation or lending. The product structure separates KAG cleanly from synthetic silver positions and from unallocated silver claims at large bullion banks. Holders can redeem against physical silver in Kinesis-supported jurisdictions, and the recent Mercado Bitcoin listing in Brazil opens a BRL on-ramp into Latin America's largest digital asset platform.

Trust Score range RWTS publishes on KAG sits in the high 80s to low 90s, weighted on custody quality (Brink's, LBMA Good Delivery), audit cadence (monthly), redemption rights (yes, with thresholds), and yield mechanism (fee-share, not lending). The risk factors we list openly: smaller market cap than gold tokens (KAG averaged $0.57 billion in monthly spot volume in 2025 per CoinGecko), redemption-jurisdiction limits, and the platform-revenue dependency of the yield mechanism.

PAXG and XAUT are gold tokens, not silver, but they sit in the same allocated-vaulted-redeemable category and earn a Trust Score in the same range for the gold side. PAXG carries NYDFS oversight and Brink's vaulting in London. XAUT runs on Tether's custody chain with Swiss vaulting. Each token represents one troy ounce of LBMA Good Delivery gold. For the gold portion of an allocation that needs an on-chain leg, both clear the institutional bar.

What we do not Trust-Score in this category: any silver token without monthly attestation, without a named custodian, without a published redemption process, or with a yield mechanism that depends on lending the underlying metal. The bar is allocated, audited, redeemable. Anything below that bar is a different product and gets a different review.

What the May Cycle Actually Tests

The May delivery cycle is a test of whether COMEX can absorb the deficit without breaking the registered-eligible separation that gives the futures contract its physical anchor. If May runs hot, registered inventory takes another step lower and the coverage ratio gets thinner going into the July contract. If May runs normal, the squeeze waits another month, but the deficit math does not change.

For a stacker holding physical, the May cycle is interesting but not directly actionable. The position is the bar. For a portfolio that holds physical and wants to add the allocated-tokenized leg for liquidity, redemption optionality, or 24/7 settlement, the May cycle is one of several setups the year will offer. The institutional citations are now stacked on the same side: the Silver Institute on supply, COMEX data on coverage, Bank of America on price.

The stacker community has been right on the trajectory. The numbers above are not RWTS opinion. They are the printed reports of the institutions that publish them.

The Bottom Line

Physical first. Tokenized second.

If you hold physical and you want to add an allocated, audited, redeemable on-chain leg to the silver portion of your allocation, RWTS publishes Trust Scores so you can compare KAG against the alternatives on the same axes we use for tokenized treasuries: custody, audit, redemption, yield source, regulatory standing.

We do not tell you whether to buy silver. We do not tell you whether COMEX will hold or break. We rate. You decide.

Related research

For the parallel allocated-and-audited tokenized gold market that KAG sits next to, see the tokenized gold $6B market cap analysis. For the broader yield-bearing RWA opportunity set, see the best RWA yield opportunities ranking. The full RWTS Trust Score methodology is on the RWTS Rating page.

Methodology: rwts.com/methodology

Not financial advice.