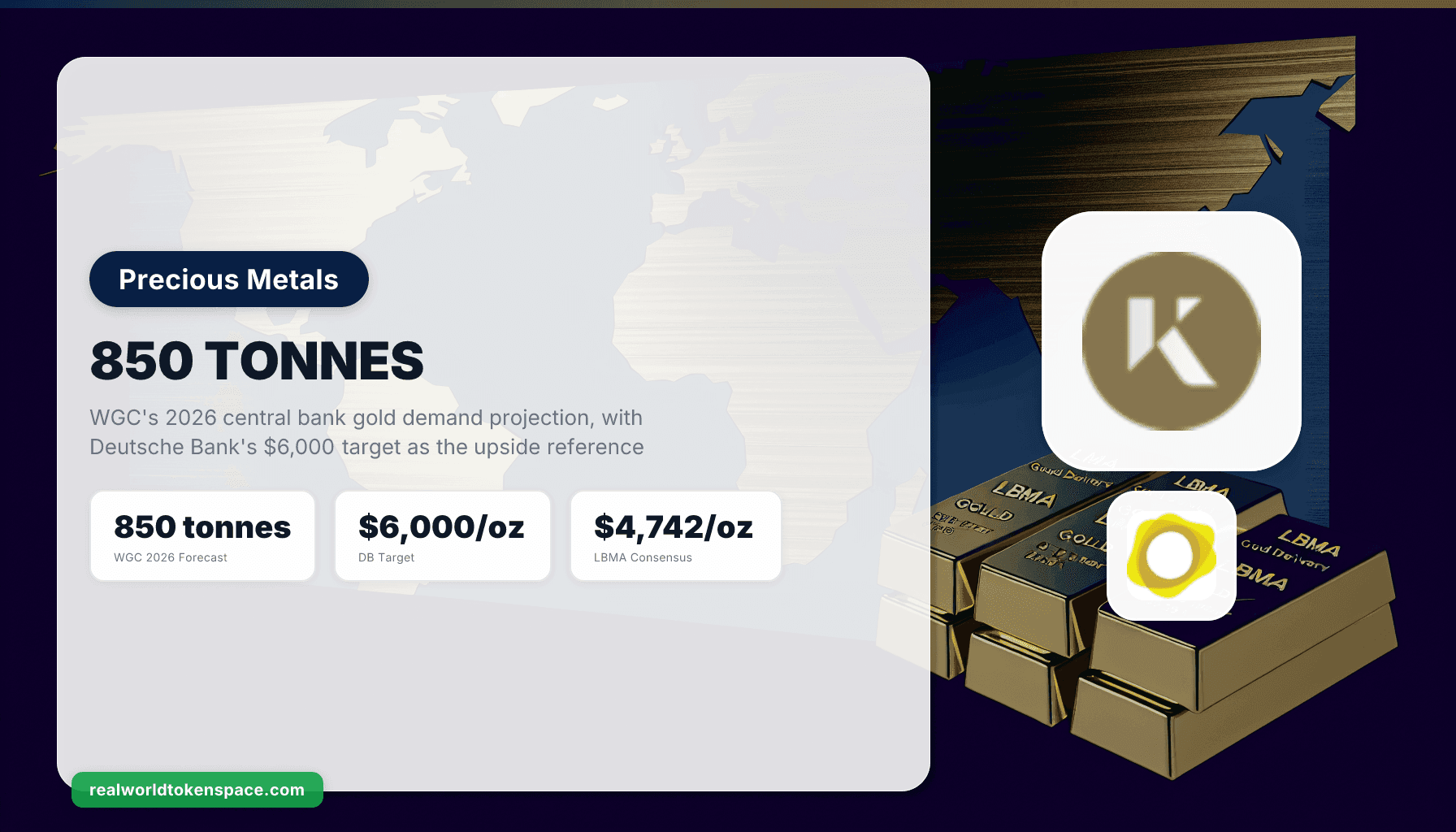

The World Gold Council's Q1 2026 Gold Demand Trends projects that central banks will purchase approximately 850 tonnes of gold during 2026. The figure tracks closely with 2025's 863 tonnes and would mark the fifth consecutive year that official sector buying exceeded 700 tonnes. For context, the average annual figure for the prior decade was 446 tonnes. The institutional demand is not slowing.

Deutsche Bank's Metals Research desk, led by Michael Hsueh, reiterated its $6,000 per ounce 2026 target on February 2, up from a previously revised $4,450 figure. With LBMA spot gold trading near $4,500 on the April 30 PM fix, the implied move is roughly 33% over the remainder of the year. The LBMA's own consensus survey of 28 analysts sits at $4,742, with a range from $4,000 to $6,050.

The buyers are diversifying. Poland led Q1 2026 with more than 20 tonnes added, the largest single-country accumulation so far this year. China and Kazakhstan continued multi-year programs. New names appeared on the buyer side: Guatemala, Indonesia, and Malaysia, the last two rejoining after long absences. Russia and Turkey were net sellers, both drawing on reserves to manage internal economic pressure rather than rotating out of the asset class.

The physical reality

Gold is doing what stackers said it would. The metal is being moved off Western balance sheets and into Asian and emerging market vaults. The "if you don't hold it, you don't own it" principle still applies, and tokenization is not a substitute for that. But for allocators who already hold physical and want a yield-bearing or fractional layer alongside the bars in their safe, the tokenized category has matured.

Tokenized gold spot trading hit $90.7 billion in Q1 2026, surpassing all of 2025 ($84.6 billion combined) per BeInCrypto's tokenized gold tracker. The growth is real, but two facts deserve emphasis. First, the on-chain category remains a rounding error against the LBMA spot market, which clears more than $200 billion per day on average. Second, tokens remain custody-dependent. Any allocator using them for sound-money reasons should factor in custodian risk on top of issuer risk.

Tokenized gold options, RWTS Trust Score

For investors who already hold physical and want a yield-bearing or fractional layer, three tokenized gold products stand out:

KAU (Kinesis Gold), Trust Score 92, Tier 1. Each KAU token represents one gram of LBMA Good Delivery gold, vaulted with Brink's, Loomis, and Malca-Amit across Sydney, London, Zurich, Singapore, and other locations. Audits run quarterly. KAU is the only product on this list that pays passive yield: roughly 0.45% APY based on a 15% share of Kinesis transaction fees, paid in KAU. Q1 2026 monthly trading volume averaged $0.57 billion. The redemption mechanic for physical bars at vault locations has worked since launch.

PAXG (Paxos Gold), Trust Score 89, Tier 1. One token represents one fine troy ounce of London Good Delivery gold, held by Brink's vaults in London under New York Department of Financial Services oversight. Q1 2026 monthly spot volume averaged $5.72 billion, the largest in the category. Redemption requires meeting Paxos's minimum bar size and settlement procedures. No yield, but the regulatory framework is the most institutional of the three.

XAUT (Tether Gold), Trust Score 86, Tier 1. One token equals one troy ounce of London Good Delivery gold held in Switzerland. Q1 2026 monthly spot volume averaged $5.32 billion. Issuer transparency is acceptable but lower than Paxos. No yield. Strong liquidity on offshore venues, weaker presence on regulated U.S. exchanges.

The Trust Score gap between KAU at 92 and XAUT at 86 reflects three things: yield mechanism (only KAU pays), custodian disclosure depth (KAU and PAXG publish vault-level attestations more frequently than Tether), and regulatory clarity (PAXG's NYDFS oversight is the cleanest, KAU's Cayman structure is acceptable, Tether's structure is the least transparent of the three).

What 850 tonnes actually means for the market

If WGC's projection holds, central banks will absorb roughly 24% of newly mined gold supply in 2026. Mine production runs about 3,500 tonnes annually and has been flat for nearly a decade despite higher prices. That alone supports a price floor above $4,000 even before accounting for ETF flows or retail buying. The real question for 2026 is whether Western central banks join the buying. So far they have not. If even one major Western reserve manager (the Fed, ECB, BOE, or SNB) begins net accumulation, the existing forecast range becomes conservative.

Watch for: WGC's mid-year demand update in July, monthly IMF International Financial Statistics filings (the official record of central bank gold movements), and any commentary from the BIS on official-sector positioning. Those are the signals that move institutional consensus, and the tokenized gold market tends to follow rather than lead.

The bottom line

Central bank buying is the most important macro signal in the metals market today. The WGC's 850-tonne projection plus Deutsche Bank's $6,000 target reflect a structural thesis: official institutions are reallocating reserves out of dollar-denominated assets and into gold. The metal is doing the work. Tokenization adds optionality (yield, fractional ownership, 24/7 settlement) for allocators who want it, but it does not replace the bar in the safe.

Physical first. Tokenized second.

RWTS isn't bullish or bearish on gold. We're the credit-rating agency for tokenized real assets. We rate. You decide.

Methodology: rwts.com/methodology. Not financial advice.

Related research

Stay Ahead of the Yield Curve

Subscribe to The Yield Report for weekly yield intelligence.

Subscribe Now