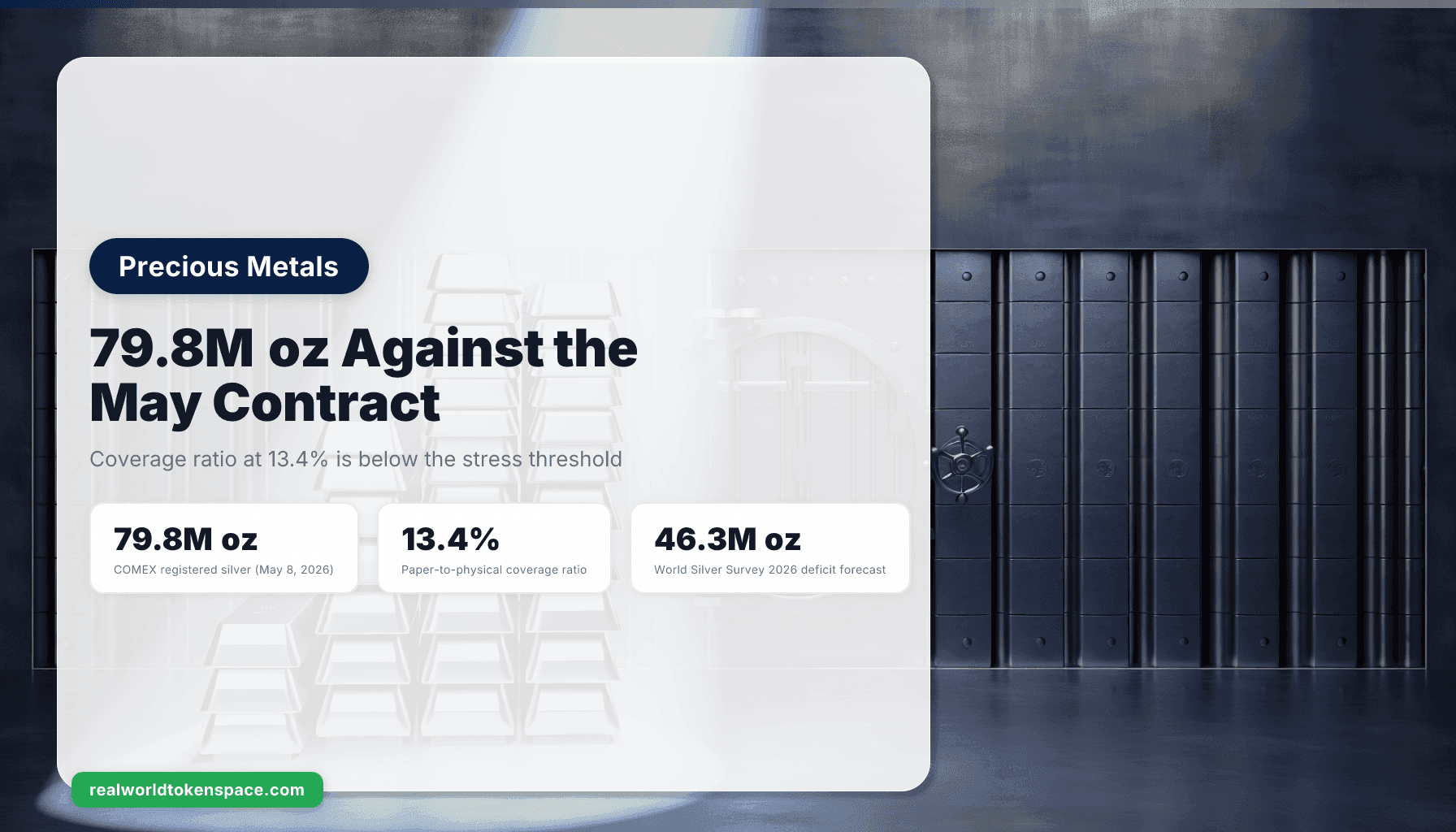

The May silver contract on COMEX is approaching First Notice Day, and the inventory math behind it tells a story stackers have been narrating for two years. As of May 8, 2026, registered silver in the COMEX system stands at approximately 79.8 million ounces. Against the open interest sitting on the May contract, that registered pool implies a coverage ratio of roughly 13.4%, which is below the stress threshold most legacy analysts use to flag a potential delivery squeeze. The paper-to-physical ratio across all open silver futures on COMEX is now around 6.3 to 1. None of these numbers, in isolation, force a delivery dislocation. Together, they describe a market where the deliverable pool is thin enough that any concentrated stand for delivery can move the price meaningfully.

The Silver Institute's World Silver Survey 2026, released earlier this quarter, projects a sixth consecutive annual physical deficit at approximately 46.3 million ounces for 2026. Bank of America, Citi, and Reuters analysts have all published 2026 silver price targets in the $200 to $300 range, with the latter end of that band tied to a tight-COMEX scenario. The institutional voices are now aligned with what the stacker community has been calling for three to four years: silver's structural supply deficit is the dominant macro story, and the inventory shrinkage at COMEX is the live signal that the deficit is biting.

What the May Contract Cycle Actually Tests

COMEX silver contracts settle in 5,000-ounce lots. When a contract holder stands for delivery, the registered inventory at approved depositories is the pool from which the warrants are drawn. Eligible inventory (silver held at COMEX depositories but not warranted for delivery) sits adjacent to registered, but only registered metal can settle a delivered contract without reclassification. The 79.8 million-ounce registered figure is what matters for the May cycle. The coverage ratio of 13.4% is calculated against the open interest still standing on May contracts at this point in the cycle. A historically normal ratio sits above 25% to 30%. Below 15%, the legacy desk reads as a tightening pool. Below 10%, the desk reads as a stress event.

The market has been here before. In January 2026, approximately 33.45 million ounces were withdrawn from registered in a single week, representing roughly a quarter of the deliverable pool at that time. That episode did not produce a default. It produced a price move and a refilling of the pool via reclassifications from eligible inventory and metal flows from LBMA refineries. The legacy plumbing held. The question for May is whether the same plumbing holds when the starting registered pool is already thinner and the deficit is six years deep.

The Mechanism, Named

Coverage ratios compress when stand-for-delivery activity outruns refinery throughput and the LBMA-to-COMEX metal flow. The lever connecting the macro deficit to the COMEX number is not paper speculation. It is industrial off-take and refinery capacity. The World Silver Survey 2026 attributes the deficit to two structural drivers: solar PV demand growing at roughly 7% to 9% annually (driven by silver paste in photovoltaic cells), and electronics demand holding firm despite cyclic softness elsewhere. The annual mine output of approximately 820 million ounces has been roughly flat for five years. Recycled supply has grown but cannot close the gap. When industrial offtake clears the LBMA market faster than miners and refiners can replace bars, COMEX registered drains as a consequence, not as a cause.

This is the structural read on what the 13.4% coverage ratio means in mechanism terms: industrial silver demand is pulling refined inventory out of the system at a pace the supply side cannot match, and the COMEX registered pool is the residual buffer absorbing the imbalance. Stand-for-delivery activity from physical buyers (industrial, refining, ETF custody) is what would convert the pressure into a price move.

Where the Conditions Bind

The 13.4% coverage ratio is a stress reading, not a default reading. If May First Notice Day arrives with stand-for-delivery activity sitting in the historical range of 1,500 to 4,000 contracts, the registered pool will likely refill via eligible reclassifications and refinery flows, and the price impact will be contained to the lease rate signal rather than a delivery dislocation. If stand-for-delivery activity prints above 5,000 contracts (roughly 25 million ounces called against a 79.8 million ounce pool), the registered buffer compresses to a level where the legacy plumbing visibly creaks and the price has to clear the spread.

A second condition is the LBMA lease rate. London silver lease rates were elevated above 5% earlier this year, indicating an unwilling lender market for refined bars. If those rates stay elevated through First Notice Day, the implication is that the refined pool at LBMA is also tight, which removes one of the buffers COMEX has historically relied on. If lease rates compress before First Notice Day, the system has more slack than the inventory headline suggests.

A third condition is the dollar. With the Fed at 3.50% to 3.75% and real Treasury yields where they currently sit, silver's directional response to a delivery event is amplified by the dollar's posture. A weaker dollar in the next two weeks would extend any silver move higher beyond the COMEX-specific drivers. A surprise dollar bid would compress the move regardless of how the contract cycle resolves.

What Stackers Already Know

The "if you don't hold it, you don't own it" frame is unaffected by any of this. Allocated bullion in private safes, in segregated storage at Brink's and Loomis, and in the LBMA Good Delivery system at named vaults is still allocated and still bears no counterparty risk to COMEX. The signal stackers should be reading from the 79.8 million ounce number is not "the system is breaking." It is "the structural deficit is now visible in the legacy plumbing, and the largest institutional analysts have caught up to where the stacker community already was."

The $300 silver target from BofA, Citi, and Reuters is not a stacker call. It is a sell-side analyst call grounded in the same deficit math the World Silver Survey reports. The institutional alignment matters because it loosens the constraint on large allocators who needed external cover before adding silver to a portfolio. The suits agree now, and that changes the marginal flow into silver-denominated allocations even if the COMEX coverage ratio rebuilds.

The RWTS Edge: Tokenized Silver, Carefully

For allocators who want a position in physical silver without managing custody (or who want a tokenized layer on top of an existing stack), the Trust Score view on the tokenized silver market is narrower than it is for gold. The category is smaller, the audit cadence is less mature, and the liquidity outside the largest products is thinner. Two products are worth naming.

KAG (Kinesis Silver) at Trust Score 90 is the cleanest read in the category. Each KAG represents 10 grams of allocated silver in the Kinesis vault network, audited monthly, redeemable into physical at vault locations, and structured similarly to KAU on the gold side. The product uses LBMA Good Delivery bars as its underlying reserve and pays a small minting yield for movement velocity. The Tier 1 designation reflects allocation quality, custody arrangements, audit cadence, and redemption mechanics consistent with the RWTS methodology.

XAGm (Matrixdock Silver) is pending Trust Score review. The product is allocated and audited under Matrixdock's framework, and the early read suggests it will land in the Tier 2 to Tier 1 band depending on how the methodology lands on its custody structure and audit cadence. We will publish a full score once the review closes.

For allocators rotating dollar reserves toward silver in response to the COMEX inventory data and the institutional alignment behind the $200 to $300 target band, KAG is the available Tier 1 option in the tokenized layer. The choice between physical allocation and a tokenized allocation comes down to liquidity, jurisdiction, and the operational question of whether the holder is set up for bar custody.

The Bottom Line

The COMEX May silver delivery cycle sits on a 79.8 million ounce registered pool against a 13.4% coverage ratio, below the legacy stress threshold. The World Silver Survey 2026 projects a 46.3 million ounce annual deficit for the sixth consecutive year. BofA, Citi, and Reuters have all published 2026 silver price targets in the $200 to $300 range. The structural deficit is now visible in the legacy plumbing.

If stand-for-delivery activity stays inside the historical range and LBMA lease rates compress before First Notice Day, the system absorbs the cycle and the price impact is limited to the lease rate signal. If stand-for-delivery activity prints heavy and lease rates stay elevated, the spread between paper and physical clears the price and the registered pool refills only at a higher level.

RWTS isn't bullish or bearish on silver. We're the credit-rating agency for tokenized real assets. We rate. You decide.

Physical first. Tokenized second.

Not financial advice.

Related research