The Senate Banking Committee released compromise text on the Clarity Act on May 1, and the version that emerged from negotiation is the most consequential regulatory event for stablecoin yield products since the GENIUS Act was signed into law in July 2025. The compromise draws a single, clean line through the stablecoin yield universe. On one side: activity-based reward programs of the type Coinbase runs against USDC are explicitly preserved. On the other side: anything that pays a yield on a stablecoin balance in a way the regulators judge functionally or economically equivalent to a bank deposit rate is prohibited.

For RWTS readers, the practical question is which products sit on which side of that line. The compromise text does not enumerate winners and losers. It draws a principles-based boundary, which means each issuer and exchange now has to argue its product into the surviving category, and allocators have to read those arguments alongside the regulatory text.

We are the credit-rating agency for tokenized real assets. RWTS does not lobby Washington and we do not predict legislation. What we can do is read the text, map it onto the products we already rate, and tell allocators where the regulatory risk concentrates.

The Compromise In One Paragraph

The Clarity Act compromise was negotiated through April by Senators Thom Tillis and Angela Alsobrooks with White House facilitation, and the public text dropped on May 1. The key provision is a carve-out that allows crypto firms to continue running rewards programs tied to "real participation on crypto platforms and networks," in the words of Coinbase chief legal officer Paul Grewal. The matching prohibition bars yield paid on stablecoin deposits where that yield would be "functionally or economically equivalent" to bank yield. Coinbase CEO Brian Armstrong's response to the compromise was a two-word public endorsement: "Mark it up." The bill is now moving toward markup, not a final-version vote, but the compromise language has stabilized enough that allocators can plan around it.

Side One: Activity-Based Rewards Survive

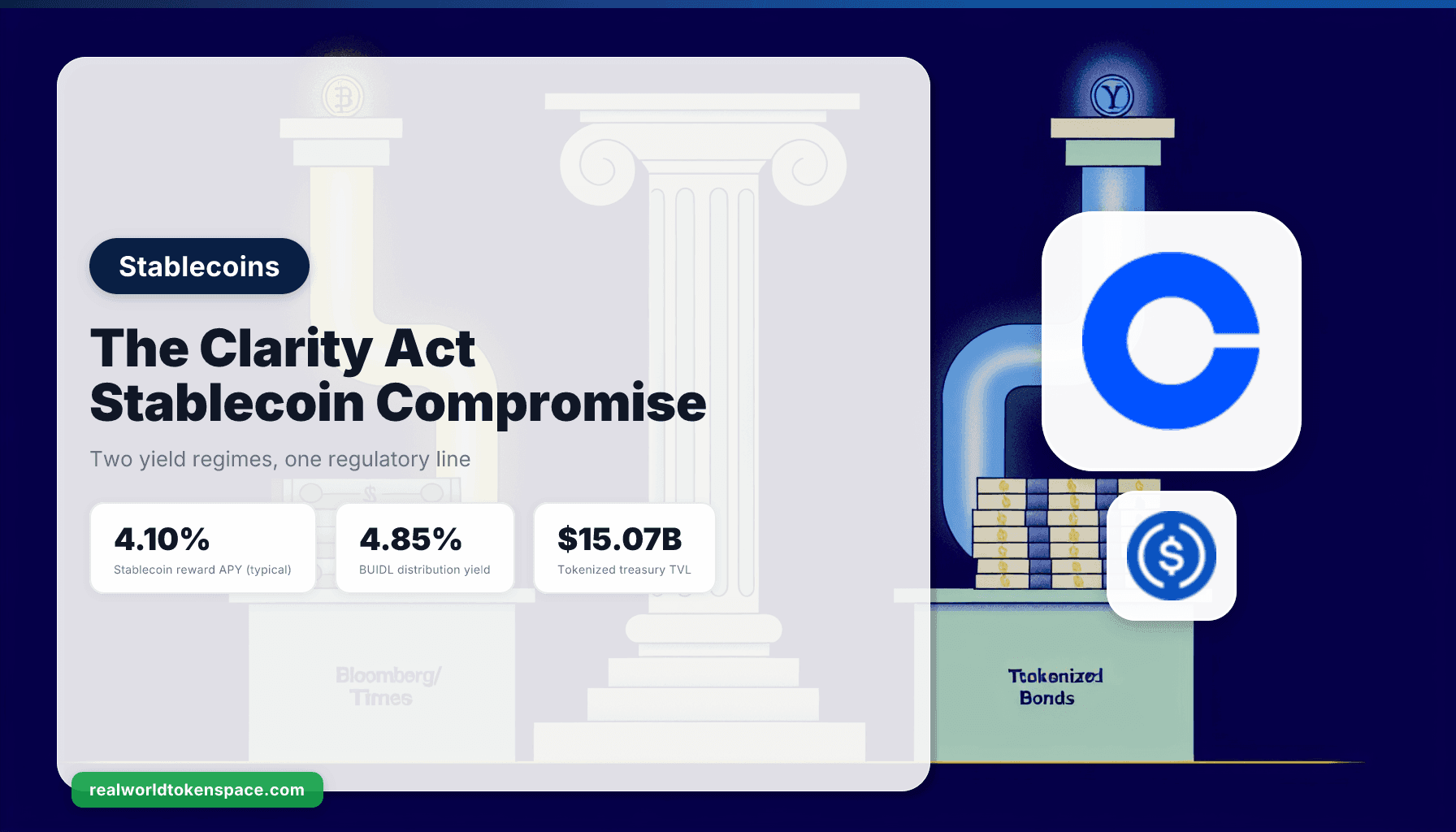

The activity-based language is the more important half of the compromise. It preserves the structure that Coinbase's onchain USDC lending program and similar exchange reward products are built on. These programs do not pay a flat APY on a stablecoin balance. They route user USDC into onchain lending markets (Morpho, in Coinbase's case, currently distributing approximately 10.8% APY on the aggregated supply rate as of early May), and the user earns a share of the actual lending revenue. The yield is not a contractual deposit rate. It is a pass-through of an underlying activity the user opted into.

The mechanism naming matters. The lever that lets these programs survive is that the yield source is observable, variable, and tied to a specific onchain activity rather than to a bank-style fixed promise. If borrowing demand on Morpho contracts, the rewards APY contracts. If lending demand expands, the APY expands. The user is not insured against rate moves and is not promised a number. Regulators reading the Clarity Act compromise can credibly distinguish that structure from a bank deposit because the economics of the two are not equivalent in any week.

For Coinbase specifically, this is the reason the company endorsed the compromise rather than fighting it. The exchange's onchain USDC product is one of the largest single contributors to its retail-side stablecoin revenue. Preserving that product was the line in the sand. The compromise lets them keep it.

Side Two: Tokenized Treasuries Are Not Stablecoins

The second category of products that benefits cleanly from the compromise is tokenized US Treasury funds. BUIDL, USDY, USYC, and OUSG are not stablecoins under the GENIUS Act framework. They are tokenized representations of underlying Treasury or money-market exposure, and the yield they distribute is the actual coupon and money-market interest the underlying portfolio earns. That yield (currently approximately 4.85% on BUIDL distribution, 4.80% on USDY, in the same range on USYC and OUSG) is a pass-through of Treasury bill rates set in the Treasury market, not a deposit rate set by an issuer.

That distinction is what keeps tokenized treasuries on the safe side of the Clarity Act line. The yield is not paid on a "stablecoin deposit." It is the economic return of the underlying fund, distributed proportionally to token holders. If a regulator asked the structural question (is this functionally equivalent to a bank deposit?), the structural answer is no: the holder owns a tokenized share of a regulated fund, the fund holds Treasury bills, and the yield is the bills' yield minus the management fee. That is the same structure money market funds have used for decades, transposed onto a tokenization wrapper.

RWTS Trust Score view on the cohort, anchored to the regulatory clarity:

BUIDL sits at a Trust Score of 88, the highest in the segment. BlackRock's brand, BNY Mellon custody, and the Securitize wrapper put the operational quality at the top. The Clarity Act compromise reduces a regulatory risk that already barely applied to BUIDL, because BUIDL is qualified-purchaser only and structured as a registered fund. The score does not move on this news, but the qualitative confidence in the product's regulatory durability moves up.

USDY carries a Trust Score of 83. USDY is the retail-accessible Ondo product, a tokenized note structure that has historically carried the most regulatory ambiguity in the cohort. The Clarity Act compromise is a meaningful tailwind here. USDY pays through the Treasury yield, not a deposit rate, and the activity-based language plus the Treasury fund carve-out together remove the most plausible adverse-interpretation scenario.

USYC, Circle's institutional cash management token, holds a Trust Score of 83 and recently overtook BUIDL as the supply leader at approximately $2.9 billion. Circle's tight integration of USYC with USDC reserves and exchange custody flows is unaffected by the compromise. If anything, the compromise validates the architectural choice to keep the cash management token structurally distinct from USDC itself.

OUSG holds a Trust Score of 86. The product is qualified-investor only at issuance, holds primarily BUIDL as its underlying vehicle, and just demonstrated end-to-end cross-border redemption infrastructure with JPMorgan, Mastercard, and Ripple last week. The Clarity Act compromise is again confirmatory rather than transformative for this score, but it removes one of the residual tail risks that allocators had been pricing in.

The Line Where The Compromise Bites

The category that loses ground in the compromise is yield-bearing stablecoin products structured as flat APY on a balance, where the issuer or platform pays a fixed-spread rate on customer deposits. This is the category most likely to fail the "functionally equivalent to bank yield" test. We do not name specific products in this paragraph because the bill is still moving toward markup and individual product structures vary, but allocators with exposure to flat-APY stablecoin yield products should re-read the structure of those products against the compromise text and ask whether the issuer can make the activity-based defense.

The mechanism that distinguishes the survivors from the losers is whether the yield source is observable activity (onchain lending, Treasury fund interest, RWA cash flows) or a contractual rate the issuer pays out of its own balance sheet. Activity passes the compromise. Contractual rates do not.

Why The Compromise Was Likely

The reason this version of the compromise was the politically achievable one is that banks were never going to accept legislation that authorized a parallel deposit-yield system on stablecoin rails. Bank lobby pressure against yield-bearing stablecoin deposit equivalents has been the single most consistent feature of the 119th Congress's stablecoin legislative trajectory. The Tillis-Alsobrooks compromise resolves that pressure by formally drawing the line where the banks wanted it drawn, while preserving the activity-based reward category that the crypto industry actually depends on.

Crypto exchanges, in turn, are net winners under this structure because their highest-margin retail product (variable-yield onchain lending tied to user opt-in) is explicitly preserved. Tokenized treasury issuers are net winners because their structural distinction from stablecoins is now more clearly recognized in the regulatory framework. The losers are flat-APY stablecoin yield products that cannot frame their yield source as activity-based.

What Allocators Should Do Now

Three actions, in order of practical priority. First, audit any flat-APY stablecoin position against the compromise text and ask whether the issuer can articulate an activity-based yield source. If they cannot, the regulatory risk on that position has just been repriced higher and the position size should reflect that.

Second, recognize that the compromise narrows the relative regulatory risk gap between tokenized treasuries and yield-bearing stablecoins. If the choice was previously USDY at 4.80% versus a flat-APY stablecoin product at 5.50%, the regulatory adjustment has just reduced the implicit yield premium the riskier product was offering. Tokenized treasuries look better on a risk-adjusted basis after this compromise than before.

Third, do not over-extrapolate to a final bill. The compromise text is the negotiation outcome at committee level, not a final-form law. Markup will introduce changes. The Senate floor will introduce changes. The conference with the House will introduce more. The directional read (activity rewards live, bank-equivalent yields die, tokenized treasuries are unaffected) is the durable signal. Specific dollar thresholds, transitional provisions, and enforcement mechanisms are still in motion.

The Bottom Line

The Clarity Act compromise validates the architectural choices that BUIDL, USDY, USYC, and OUSG made when they structured themselves as tokenized funds rather than yield-bearing stablecoins. It validates the architectural choice Coinbase made when it structured its onchain USDC product as a Morpho-routed activity rather than a fixed APY. It does not validate flat-APY stablecoin yield products, and allocators should reread that category through the compromise lens.

RWTS isn't bullish or bearish on any of these tokens. We rate. You decide. The compromise gives us cleaner data to score against.

Not financial advice.

Related research